Bitcoin Lending Landscape

Mapping 15+ platforms shaping the future of Bitcoin-backed borrowing

Lending is one of the most important financial primitives for Bitcoiners. The ethos of Bitcoin has always been to hodl for the long term and pass it on across generations, a hedge against the inflationary nature of fiat monetary systems. In countries hit by repeated episodes of hyperinflation, Bitcoin has often been nothing short of a lifeline.

But hodling doesn’t mean sitting idle. Increasingly, Bitcoiners are looking to borrow stablecoins or fiat against their BTC, unlocking liquidity without selling. That makes lending a “star primitive” for Bitcoin’s next growth phase.

I recently mapped the Bitcoin lending landscape and compared players across several factors. You can find the full table, but here I’ll summarize my takeaways and highlight why the space still lacks true innovation.

How I compared the players?

I grouped all platforms in the list under a few key lenses:

Basic details – founding year, location, legal setup

Trust model – custody setup (self, third-party, decentralized)

Rehypothecation – whether your BTC is re-used by the lender

Loan terms – LTV, APY, minimums, fees

Liquidation practices – how margin calls and liquidations are handled

#1. Market maturity timeline

Today, there are 15+ active platforms still servicing Bitcoin-backed lending. That’s a healthy ratio, especially in an industry where many projects don’t last beyond one cycle.

Notably, some CeFi players have been long-standing, operating reliably across multiple bull and bear markets. That consistency shows both the stickiness of demand and the durability of lending as a use case.

The broader pattern still holds: each bull market has given birth to a wave of new platforms, and a handful survive into the next.

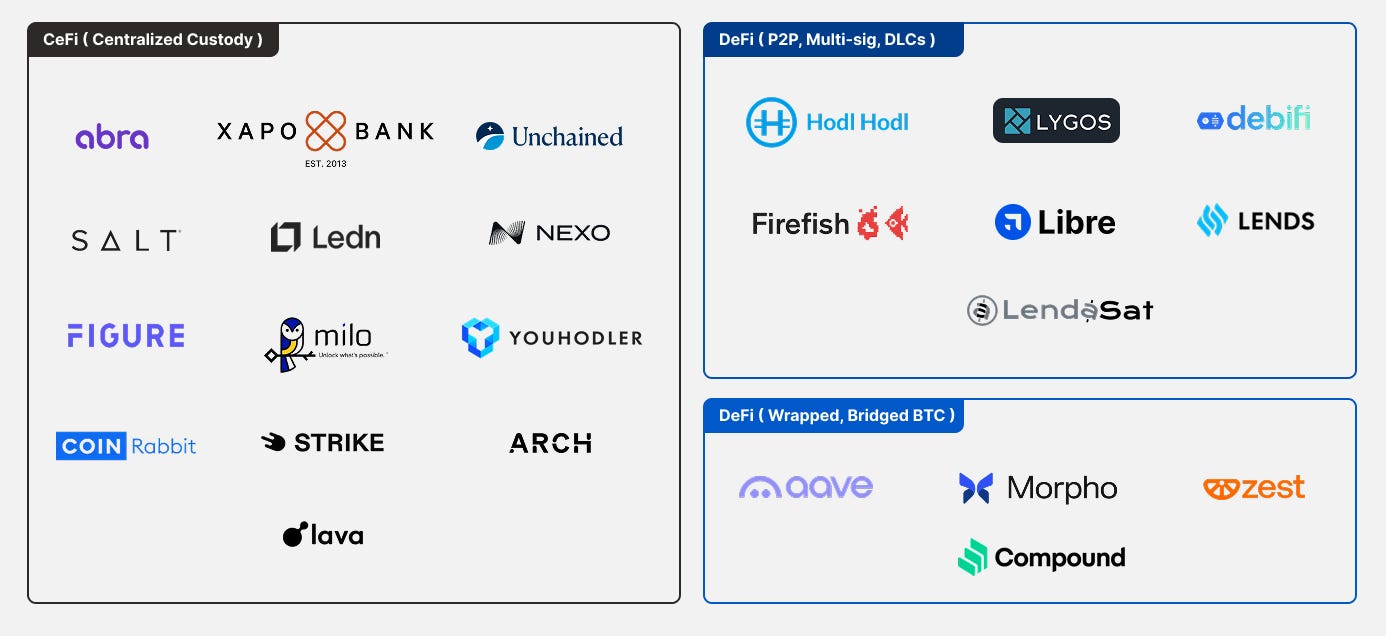

#2. Centralized players still dominate

Most platforms today remain centralized custodians, taking control of your BTC either internally or via third-party providers like BitGo or Anchorage. This model works, but it runs counter to Bitcoin’s ethos of “your keys, your coins.”

The alternatives are starting to take shape:

Decentralized and P2P models powered by multi-sigs, discreet log contracts (DLCs), and some early Taproot-based innovations.

These setups aim to remove the single point of custody while still enabling collateralized borrowing.

A quick clarification: wrapped BTC in DeFi is not fully decentralized. While it enables BTC liquidity on Ethereum and other chains, it ultimately depends on centralized custody at its origin. So while it’s widely used in DeFi, it doesn’t belong in the same category as native decentralized lending.

The collapse of BlockFi, Voyager, and FTX shook confidence in centralized models across crypto. While Bitcoin-specific lenders haven’t collapsed in the same way, the pressure to evolve toward more transparent and trust-minimized solutions is clear.

#3. Regulation and Compliance drive the Map

Most CeFi players are U.S.-based. That makes sense: the U.S. is home to a huge share of Bitcoiners, and it’s a primary market. But it also means strict oversight—money transmitter licenses (MTLs), MSB registrations, BitLicense, and more.

This has two consequences:

Higher borrower costs – licensing and compliance overhead is passed on to users.

Reliability – U.S.-regulated lenders have avoided the catastrophic collapses seen offshore.

Regulation is a double-edged sword: it makes platforms safer, but it also makes them expensive and less aligned with Bitcoin’s open ethos.

#4. Borrowing is expensive

Looking across the table, the cost of borrowing (APY, fees, minimum loan amounts) is consistently high. This stems from:

CeFi dominance with heavy operational overhead.

Limited programmability on Bitcoin itself, which reduces efficiency and competition.

The good news: with stablecoin adoption accelerating and Bitcoin infrastructure improving, the market is set up for disruption. More competition could push borrowing costs down and open the door to broader innovation.

#5. Lending isn’t for everyone (Yet)

So far, most platforms have targeted HNWI and institutions. Loan minimums and terms reflect that focus.

That creates exclusion, but it’s also natural, since large borrowers are easier to serve under regulatory and operational constraints.

As Bitcoin adoption grows through ETFs, corporate treasuries, and grassroots hodlers, the demand for retail-friendly lending products will only increase. Borrowing against Bitcoin isn’t about flipping for short-term gains; it’s about unlocking liquidity while holding BTC for the long run.

This creates space for new entrants to build accessible, decentralized, and transparent lending solutions.

Closing thought

Bitcoin lending is still in its early innings. Today’s landscape is dominated by centralized players shaped by regulation and overhead, but the demand for decentralized, trust-minimized alternatives is building.

The next bull market could be the catalyst for real innovation:

Lower borrowing costs

Custody models without middlemen

Broader accessibility for everyday Bitcoiners

Bitcoin is for everyone, and lending as a star primitive needs to evolve to reflect that.

Disclaimers

This article was written with editorial assistance from ChatGPT 5. All ideas, research, and conclusions are my own